Written by

Director Energy & Net Zero

Rainmaking

Total greenhouse gas (GHG) emissions measurement (scopes 1-3) must be thought of as an essential capability for every single business. There are three key drivers behind this:

Since 2019, large businesses have had to disclose annual UK energy use and associated greenhouse gas emissions. From 6 April 2022, over 1,300 of the largest UK-registered companies and financial institutions will have to disclose climate-related financial information on a mandatory basis. This will include many of the UK’s largest traded companies, banks and insurers, as well as private companies with over 500 employees and £500 million in turnover. And this is just the start. Increasingly, companies will need to carry out climate-related reporting to satisfy legal requirements, customers and their financiers.

Reliable measurement is key to controlling progress to net zero. It will be a key capability for any business with a clear commitment to getting to net zero, such as the 2,000+ companies with science-based emissions reduction targets (a number that’s growing at 65% year-on-year).

Unreliable measurement and reporting can leave businesses exposed. Google recently hit headlines for omitting 60% of their emissions from their reporting and claims, leaving their commitment to “Carbon Neutral since 2007. Carbon free by 2030” in question.

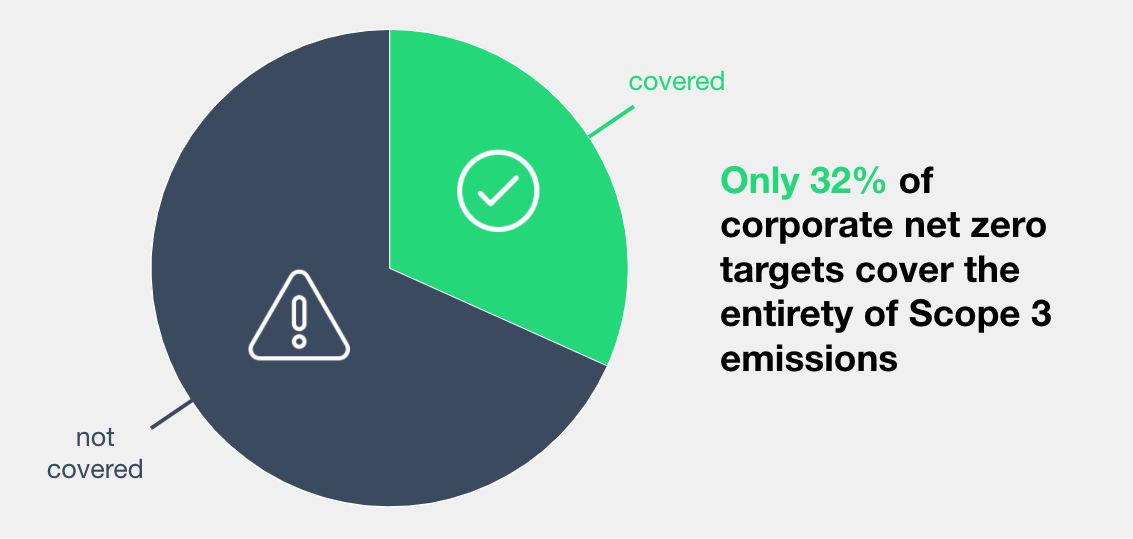

Despite drivers, 76% of companies are unable to measure the full carbon footprint of their products and services. It’s less surprising when we consider their Scope 3 emissions, which are the hardest to measure and account for more than 70% of their total emissions. Often compounding the problem are the approaches and tools being used: Some 86% of companies still record and report their emissions manually using spreadsheets. This is not scalable or efficient.

Perhaps more concerning is that we’re misrepresenting reality. According to an analysis by The Washington Post, the gap in underreported GHG emissions “ranges from at least 8.5 billion to as high as 13.3 billion tons a year.” It’s a complex area and challenges are varied; from data quality issues to siloed platforms and inconsistent measurement methodologies, challenges make it difficult to compare, combine and share reliable data. Add to the picture the opaque and unreliable nature of many offsets, and we can see how the question of net climate impact is very hard to answer with a high degree of confidence for business and industry.

Source: Zerotracker

But there are ways forward, if we can think big and radically about how we tackle these challenges. Emerging solutions from the startup ecosystem are unlocking new measurement and management potential. From Unicorns, to Series A startups; their new technologies and fresh approaches can help us to unlock this critical business capability at pace. Industry players can create more immediate business value by partnering with startups who have solutions in this space, combining the best of startup solutions with corporate scale and expertise.

Take the example of Everimpact. Rainmaking identified the potential of Everimpact to help Shell and Wilhelmsen measure and understand CO2 emissions for effective reporting and emissions analysis. A partnership was designed and initiated by Rainmaking to enable Everimpact’s proprietary and highly accurate CO2 emissions measurement solutions to be applied to ships’ emissions, enabling new levels of insight and precision by combining satellite and ground data.

And now is the time to look for innovative emerging solutions, as we’re seeing funding and solutions accelerate. VC funding into carbon footprint awareness technologies has been growing +328% CAGR over the past 3 years. These technologies and solutions received nearly 8x funding in 2021, when compared to 2020 [Source: Tracxn 2022]. Capital is being deployed by both VCs and CVCs to fuel the growth of these solutions, the majority of which are achieving Seed & Series A rounds.

To share some notable examples: Emitwise raised 7M USD seed in 2021 for its AI platform measuring GHG emissions across the supply chain; Pachama raised 15M series C in 2021 for their carbon offsets validation and marketplace solution, backed by Breakthrough Energy Ventures, Amazon and Lowercarbon Capital; and earlier this year Watershed, a San Francisco, CA-based platform helping companies track and reduce their carbon emissions, raised 70M USD in Series B funding from Kleiner Perkins and Sequoia which values the company at over 1B USD.

It’s not just the startups and VC’s who are driving the activity. Corporates are a key driver in the growth of this space as they are the ones with the pressure to integrate solutions, and they are getting their hands dirty too. For example: Kellogs are engaging with 75% of their Tier 1 suppliers to report on scope 3 emissions and enable their reduction by 20% to 2030; Daimler have started to pilot the use of blockchain technology to track the emissions of their automotive parts throughout the supply chain; and Unilever is building a system through which suppliers can share the carbon footprint of their goods and services, to ensure they meet company standards and to form a comprehensive scope 1-3 view.

So what new solutions will you bring to your industry? How might you partner with emerging startups to do so? Where would you start?