Written by

Director Energy & Net Zero

Rainmaking

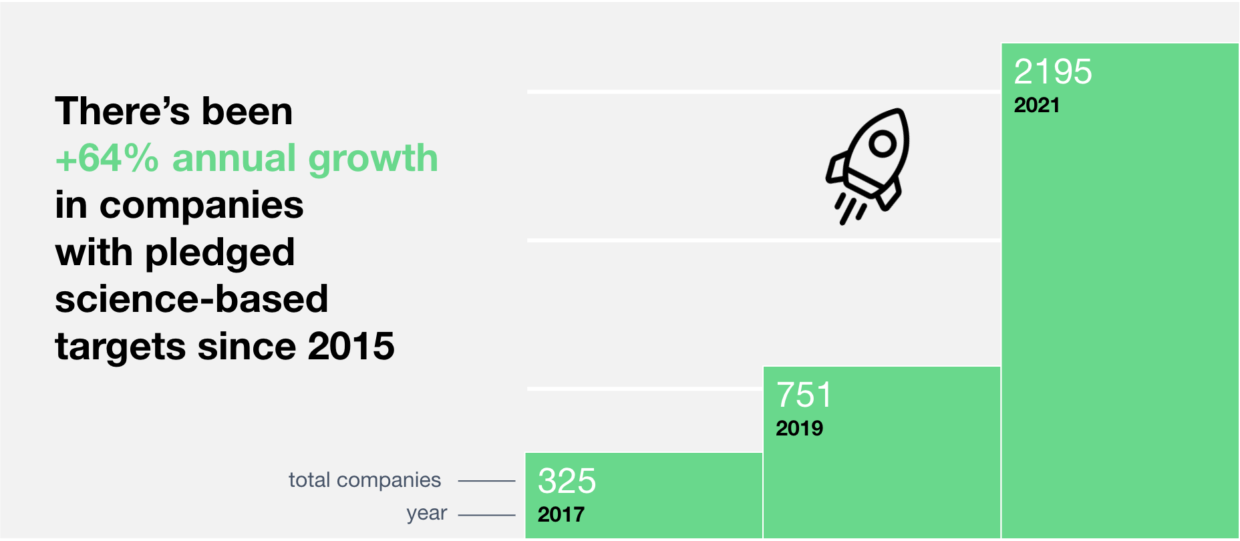

In 2019, national pledges covered 10% of global emissions (29 countries). Just two years later, 78% of global emissions are covered by net zero commitments* (92 countries). At the corporate level, more than 2,000 companies have now pledged science-based emissions reduction targets, up from just 116 in 2015. That’s +65% year on year growth.

*These are clear commitments either in law, in policy documents, officially declared or already achieved.

The level of ambition and attainment is in some cases amazing (not all of course). Here are a few of the frontrunners:

Such commitments are having a snowball effect. In the automotive sector, commitments by large automakers have resulted in a wave of auto suppliers following suit in their wake. They are wrapped up in each others’ supply chains so must all move together to have any chance of impact on scope 3 emissions. To give an example, ZF, a major automotive parts manufacturer, committed to net zero across scopes 1-3 by 2040 following a similar commitment by Mercedes several months earlier.

Source: SBTi

Across regulation, customer demand, competition and technology, the shift towards net zero occurs at a rate that continually outpaces expectation. The result? We continually overestimate future fossil fuel demand (such as peak-oil volume and timing), leading to stranded fossil-fuel assets. The flip-side is that we continually underestimate the future scale of renewable energy, and may frequently be missing opportunities as we’ve perceived timing not to be right. Take the recent example of Uniper, a German utility who brought its last new coal power plant online in 2020. Shortly after its launch, the German government announced plans to exit coal; initially by 2038, and now brought forward to 2030. This will leave the powerplant with just 10 years of operation; less than a quarter of its 45-year design life. And for renewables, today the BNEF forecasts 85% of global primary energy will be renewable by 2050, whereas in 2011 the EIA were forecasting this figure to be just 25%. In the latter example, expectations were out by a factor of 3x and this keeps happening.

It’s evident that the pace of change is difficult to forecast when it comes to net zero and enabling technologies. Emerging signals can help us to take a more evidence based approach when trying to understand what might be coming and how quickly. Let’s take a very big signal; startup unicorns. These are privately owned start-ups reaching USD 1B valuations. There are currently 43x private, USD 1B+ climate tech companies (Q1 2022). A whopping 60% of them reached unicorn status in 2021, showing us that the amount of climate tech unicorns is accelerating. In addition, climate tech unicorns have been reaching their USD 1B valuation faster than the average. The average time to reach unicorn status is 7 years; climate tech startups now take under 4. Yep, 0 to $1bn valuation in under 4 years.

Source: Climate Tech VC

Digging deeper, investment into startups can reveal where growth is concentrated and momentum is building. As an example, venture funding into renewable energy technology reached USD 2.2B in 2021. This is 3x the figure in 2020 and it’s a figure that has been growing at an astounding 43% CAGR over the past 3 years to 2021. This is amazing growth, but it looks quite modest next to the emerging field of carbon emissions measurement and visibility, which over the last 3 years has been growing at 328% CAGR [Source: Tracxn 2022].

Understanding and responding decisively to early signals can help large organisations to stay ahead of the curve. That’s why clients and collaborators come to us for help in translating these early signals into business opportunities. How closely are you looking? How might you play in these emerging markets? Where can you leverage unfair advantages?